The Goods and Services Tax (GST) revolutionized India’s tax landscape, impacting various sectors, including the logistics industry. While simplifying the tax structure, GST introduced complexities regarding intra-state and inter-state movement of goods. In this detailed guide, we aim to demystify the complexities of the GST regime as it applies to logistics companies in India. We will delve into the nuances of how GST impacts both intra-state and inter-state movement of goods. Our goal is to provide clear, actionable insights that can help these companies navigate the GST landscape effectively.

Understanding GST Basics:

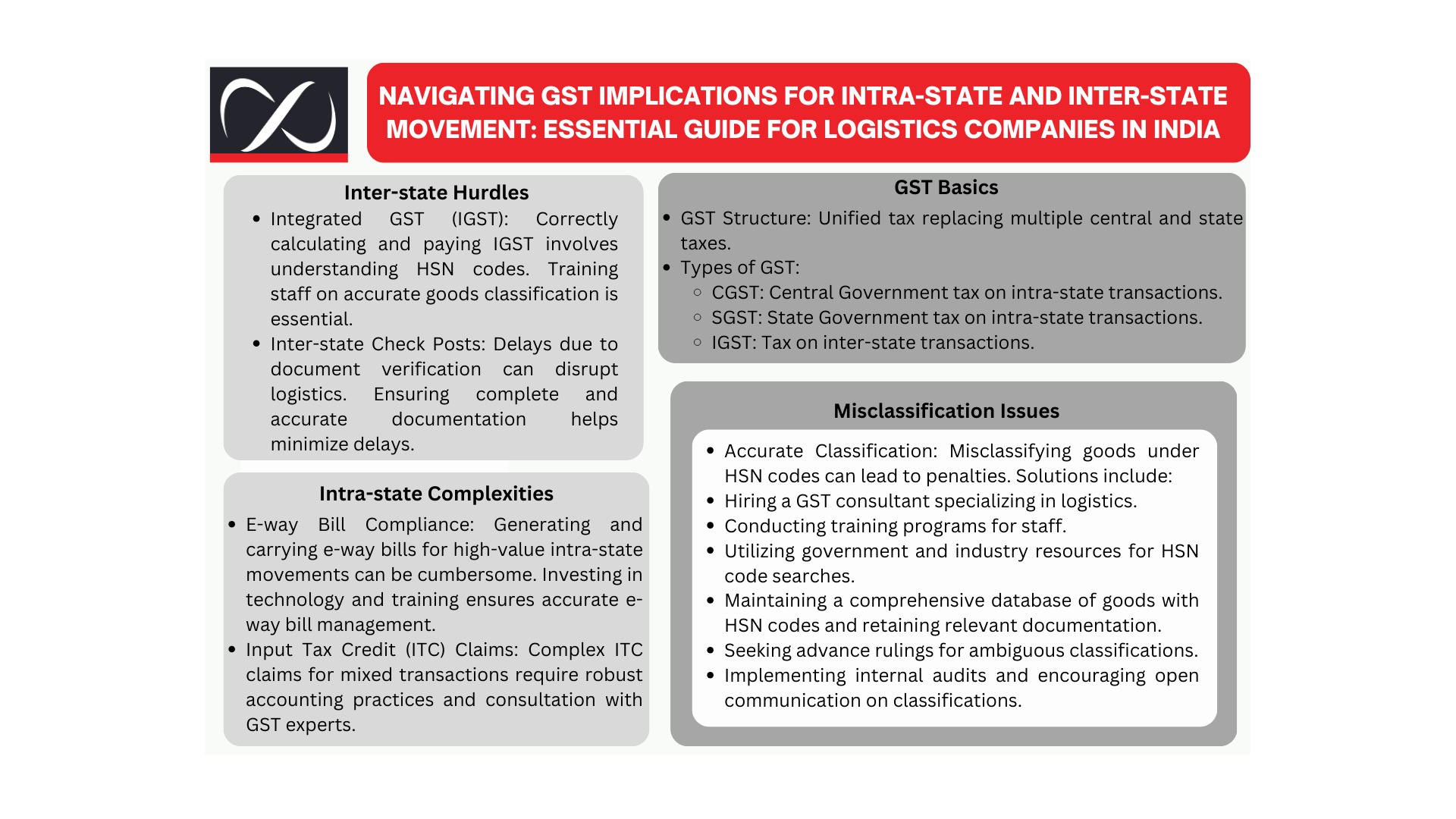

- Goods and Services Tax (GST) is a unified indirect tax levied on the supply of goods and services across India. It replaced multiple taxes levied by the central and state governments, simplifying the tax structure and fostering economic integration.

- GST is categorized into Central GST (CGST) levied by the central government, State GST (SGST) levied by the state governments on intra-state transactions, and Integrated GST (IGST) applicable to inter-state transactions.

- GST is levied at multiple stages of the supply chain, from manufacturing to distribution and consumption. Logistics companies play a crucial role in facilitating the movement of goods across different states and ensuring compliance with GST regulations.

The Goods and Services Tax (GST) has transformed the Indian logistics landscape, but challenges remain for companies navigating intra-state and inter-state movement of goods. Here’s a glimpse into some key issues:

Intra-state complexities:

- E-way bill compliance: Accurately generating and carrying e-way bills for intra-state movement exceeding a specific value can be cumbersome for smaller logistics companies with limited technological infrastructure.

- Input Tax Credit (ITC) claims: Claiming ITC on intra-state purchases can be complex, especially for companies with mixed intra-state and inter-state transactions.

Inter-state hurdles:

- Integrated GST (IGST): Calculating and paying the correct IGST rate on inter-state movement requires understanding the intricacies of the Harmonized System of Nomenclature (HSN) codes for accurate classification of goods.

- Reverse Charge Mechanism (RCM): In certain cases, the logistics company becomes liable for paying GST under the RCM. Understanding when RCM applies and adhering to its compliance requirements can be challenging.

- Inter-state check posts: Delays at inter-state check posts due to document verification can disrupt logistics timelines and increase operational costs.

These complexities can lead to penalties for non-compliance, impacting a logistics company’s financial health and reputation. To navigate these challenges, companies should invest in GST compliance software, train staff on GST regulations, and maintain meticulous documentation for all transactions. Collaborating with tax advisors experienced in logistics can also be highly beneficial. By staying informed and adopting a proactive approach, logistics companies can navigate the GST landscape efficiently and ensure a smooth flow of goods across India.

Challenge: Misclassification Issues: Accurately classifying goods under the Harmonized System of Nomenclature (HSN) code is crucial for determining the applicable GST rate. However, the sheer variety of goods transported can lead to misclassification, potentially resulting in penalties and disputes with tax authorities.

Solution:

- Investing in Expertise:

- Engaging a GST Consultant: Partnering with a qualified GST consultant specializing in logistics can provide invaluable guidance on classifying goods. Their expertise in interpreting HSN codes and understanding the nuances of GST regulations offers a safety net against misclassification.

- Training Programs for Staff: Invest in training programs for your logistics personnel, particularly those involved in shipment documentation. Empowering them with a basic understanding of HSN codes and classification principles empowers them to identify potential issues and seek guidance when needed.

- Utilizing Classification Tools:

- Government Resources: Leverage online resources provided by the government, such as the GST portal, which offer HSN code search functionalities and classification tools. These tools can be a valuable first step in identifying the relevant code for your goods.

- Industry Associations: Many industry associations provide resources and support for GST compliance. These resources may include classification guides tailored to specific industry segments, aiding in accurate categorization of commonly transported goods.

- Maintaining Detailed Records:

- Product Descriptions and Classifications: Maintain a comprehensive database of the goods you transport, including detailed descriptions and their associated HSN codes. This database serves as a quick reference point for staff and facilitates consistent classification practices.

- Document Retention: Retain all relevant documentation related to goods transported, including invoices, bills of lading, and e-way bills. This documentation is crucial for supporting your classification decisions in case of an audit or dispute with tax authorities.

- Seeking Advance Rulings:

- Clarification for Ambiguous Cases: For goods with ambiguous classifications, consider seeking an advance ruling from the tax authorities. This formal ruling provides clarity on the applicable HSN code, offering peace of mind and reducing the risk of future disputes.

- Building a Culture of Compliance:

- Internal Audits and Reviews: Implement internal audit procedures to regularly review classification practices within your logistics company. Identifying inconsistencies and addressing them proactively minimizes the risk of misclassification.

- Open Communication Channels: Encourage open communication among staff regarding product classifications. Empower personnel to raise concerns about potential misclassification and seek clarification from designated personnel or the GST consultant.

In summary, logistics companies operating in India need to navigate the implications of GST for both intra-state and inter-state movement of goods. Compliance with GST regulations, accurate tax calculations, and proper documentation are imperative to avoid penalties and ensure smooth logistics operations. Understanding the nuances of GST taxation and compliance requirements is essential for logistics companies to thrive in the dynamic business environment of India’s logistics industry.

Compliance and Documentation:

Compliance with GST regulations requires meticulous record-keeping, timely filing of returns, and adherence to invoicing requirements.

Logistics companies must maintain accurate records of invoices, e-way bills, and other relevant documents to demonstrate compliance with GST regulations during audits or inspections.

Regular training and updates on changes in GST laws and regulations are essential to ensure that logistics staff are well-informed and equipped to navigate the complexities of GST compliance effectively.

Conclusion:

In conclusion, understanding the GST implications for intra-state and inter-state movement is essential for logistics companies operating in India. By grasping the fundamental concepts of GST, adhering to compliance requirements, and leveraging technology for seamless documentation and record-keeping, logistics companies can ensure accurate tax calculations, mitigate risks, and avoid penalties. With a proactive approach to GST compliance and a commitment to staying abreast of regulatory changes, logistics companies can streamline their operations, enhance efficiency, and thrive in the dynamic business landscape of India’s logistics industry.