Introduction

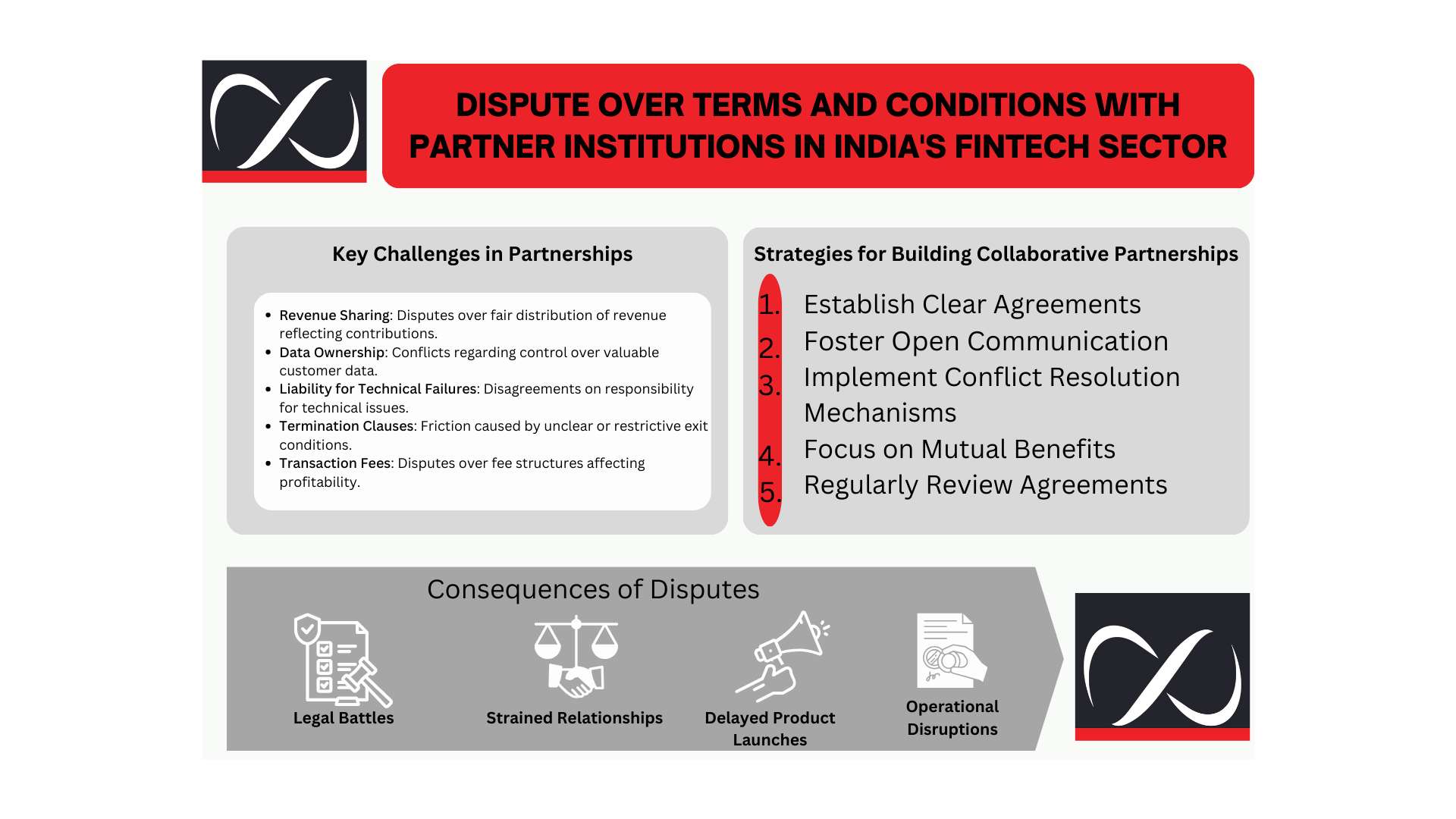

The collaboration between fintech startups and established financial institutions in India is often fraught with challenges, particularly concerning the terms and conditions of partnership agreements. Five primary issues frequently arise: revenue sharing, data ownership, liability for technical failures, termination clauses, and transaction fees. Each of these areas can lead to significant disputes, hampering the smooth operation and growth of fintech companies. In this article, we will delve into these problems, providing a detailed analysis of each, and discuss potential solutions to mitigate these challenges.

Detailed Elucidation of Problems

Revenue Sharing:

Revenue sharing agreements are a fundamental aspect of fintech-bank partnerships. The challenge lies in negotiating a fair split that reflects the contributions of both parties. For example, a fintech startup that developed an app to streamline online transactions partnered with a major bank. The startup claimed its technology attracted thousands of new users, demanding a higher share of the revenue. Meanwhile, the bank argued that its extensive network and customer trust were crucial for the app’s success. This disagreement led to prolonged negotiations, delaying the launch of the app’s new features.

In another instance, a fintech firm specializing in peer-to-peer lending faced challenges in revenue sharing with a partnering financial institution. The fintech argued that its algorithm significantly reduced default rates, justifying a larger revenue share. The bank, however, felt its regulatory expertise and customer base warranted a higher share of the profits. This impasse affected the rollout of new lending products, highlighting the need for transparent negotiations and a clear understanding of each party’s value addition to resolve such disputes.

Data Ownership

Data ownership is another contentious issue in fintech-bank partnerships. Customer data is a valuable asset, and both parties typically want control over it. In one case, a fintech company specializing in credit scoring using alternative data partnered with a traditional bank. The fintech firm wanted to retain ownership of the data it collected to refine its algorithms and expand its services. However, the bank insisted that as the primary customer interface, it should own the data to ensure compliance with regulatory standards. This conflict escalated to legal consultations, straining the partnership.

A similar scenario unfolded when a fintech firm providing personalized investment advice clashed with its banking partner over data control. The fintech startup argued that its sophisticated data analytics provided valuable insights that justified its claim to data ownership. The bank, on the other hand, believed that controlling customer data was essential for regulatory compliance and maintaining customer trust. Establishing clear data governance policies and mutually beneficial data-sharing agreements can help mitigate these conflicts and ensure a smooth collaboration.

Liability for Technical Failures

Technical failures are inevitable in the fintech sector, given the reliance on complex software and digital infrastructure. Determining liability when these failures occur can be a major source of disputes. A payment gateway provider experienced a system outage during a peak shopping period, resulting in transaction failures. The partner bank demanded compensation, claiming the fintech’s technology was responsible. The fintech company argued that the bank’s outdated infrastructure contributed to the problem. This dispute led to a temporary suspension of services, affecting customers and revenues.

Another example involves a fintech startup offering blockchain-based solutions to a bank. When a security breach occurred, the bank held the fintech responsible, citing inadequate safeguards. The fintech firm countered that the bank’s insufficient integration with the blockchain system was the root cause. This conflict resulted in a prolonged blame game, disrupting the partnership. Clear contractual agreements outlining each party’s liability and procedures for addressing technical failures are essential for preventing and resolving these disputes.

Termination Clauses

Termination clauses in partnership agreements can also lead to disputes. These clauses dictate the conditions under which a partnership can be ended, and ambiguities or overly restrictive terms can cause significant friction. A fintech firm offering lending solutions faced issues when its partner bank decided to terminate the agreement due to regulatory pressures. The fintech company contested the termination, citing insufficient notice and lack of alternative arrangements for their customers. This disagreement resulted in a lengthy legal battle, disrupting services and affecting customer trust.

In a different case, a fintech startup providing automated financial advice had a termination clause dispute with its partner bank. The startup wanted the flexibility to exit the partnership if their technology did not achieve expected results. The bank, however, insisted on strict conditions to safeguard its investment. This led to protracted negotiations and strained relations between the two parties. Crafting clear, balanced termination clauses that protect both parties’ interests is crucial for maintaining a healthy partnership.

Transaction Fees

Transaction fees are a critical revenue stream for fintech companies, but disagreements over these fees can strain partnerships. In one instance, a digital wallet startup partnered with a bank to facilitate seamless fund transfers. The startup initially agreed to a transaction fee structure but later found the fees unsustainable as their transaction volume grew. The bank was reluctant to renegotiate, leading to financial strain for the startup and a subsequent drop in service quality.

A similar dispute arose between a fintech firm offering international money transfer services and its banking partner. The fintech company argued that the high transaction fees imposed by the bank made its service less competitive in the market. The bank, on the other hand, maintained that the fees were necessary to cover compliance and operational costs. This standoff affected the growth of the fintech’s customer base and market share. Regular reviews and transparent fee structures can help align expectations and prevent conflicts.

Conclusion

The fintech sector in India faces significant challenges in navigating partnerships with established financial institutions. Addressing disputes over revenue sharing, data ownership, liability for technical failures, termination clauses, and transaction fees requires clear, transparent agreements and proactive conflict resolution mechanisms. By focusing on mutual benefits and maintaining open lines of communication, fintech startups and banks can foster collaborative relationships that drive innovation and growth in the financial sector.

Calls to Action

- Establish Clear Agreements: Ensure all terms and conditions are explicitly defined and agreed upon to prevent misunderstandings.

- Foster Open Communication: Maintain regular dialogue between fintech startups and partner banks to address concerns promptly.

- Implement Conflict Resolution Mechanisms: Develop mechanisms to resolve disputes quickly and fairly without resorting to litigation.

- Focus on Mutual Benefits: Align partnership goals to ensure both parties benefit from the collaboration.

- Regularly Review Agreements: Periodically revisit and revise agreements to reflect changing market conditions and partnership dynamics.

Addressing common points of contention—revenue sharing, data ownership, liability for technical failures, termination clauses, and transaction fees—requires careful planning and negotiation. By establishing clear, fair agreements and fostering open communication, fintech startups and banks can build strong, collaborative relationships. Conflict resolution mechanisms should be in place to handle disputes efficiently, and both parties must focus on achieving mutual benefits. Regularly reviewing and updating partnership agreements will ensure they remain relevant and beneficial in a rapidly evolving financial landscape. With these strategies, the Indian fintech sector can overcome partnership challenges and continue to innovate and grow, ultimately benefiting the broader economy.