A few weeks after SEBI unsealed its interim corporate governance order against gold processor Rajesh Exports Limited (REL), a secondary asset liquidation event deserves urgent institutional scrutiny. For an international law firm weighing India market entry through the corridor rather than through a desk, it is also a sharper worked example of SEBI reform’s cross-border legal market implications than any conference panel.

Canara Bank has officially put its INR 509.37 crore credit exposure to the embattled conglomerate up for sale via an auction process, demanding bids on a 100 per cent upfront cash basis. On its face, this reads as an ordinary domestic distressed-debt transaction: a state-run lender clears a non-performing loan, and a special-situations buyer takes on the position at a steep discount to pursue the corporate borrower and its personal guarantors. Indian non-performing asset (NPA) desks process these frameworks continuously.

What makes this exposure dangerous is the geometric disconnect between the originating default and the actual location of the realisable asset base.

India-Singapore-Switzerland-Valcambi-Gulf Nexus

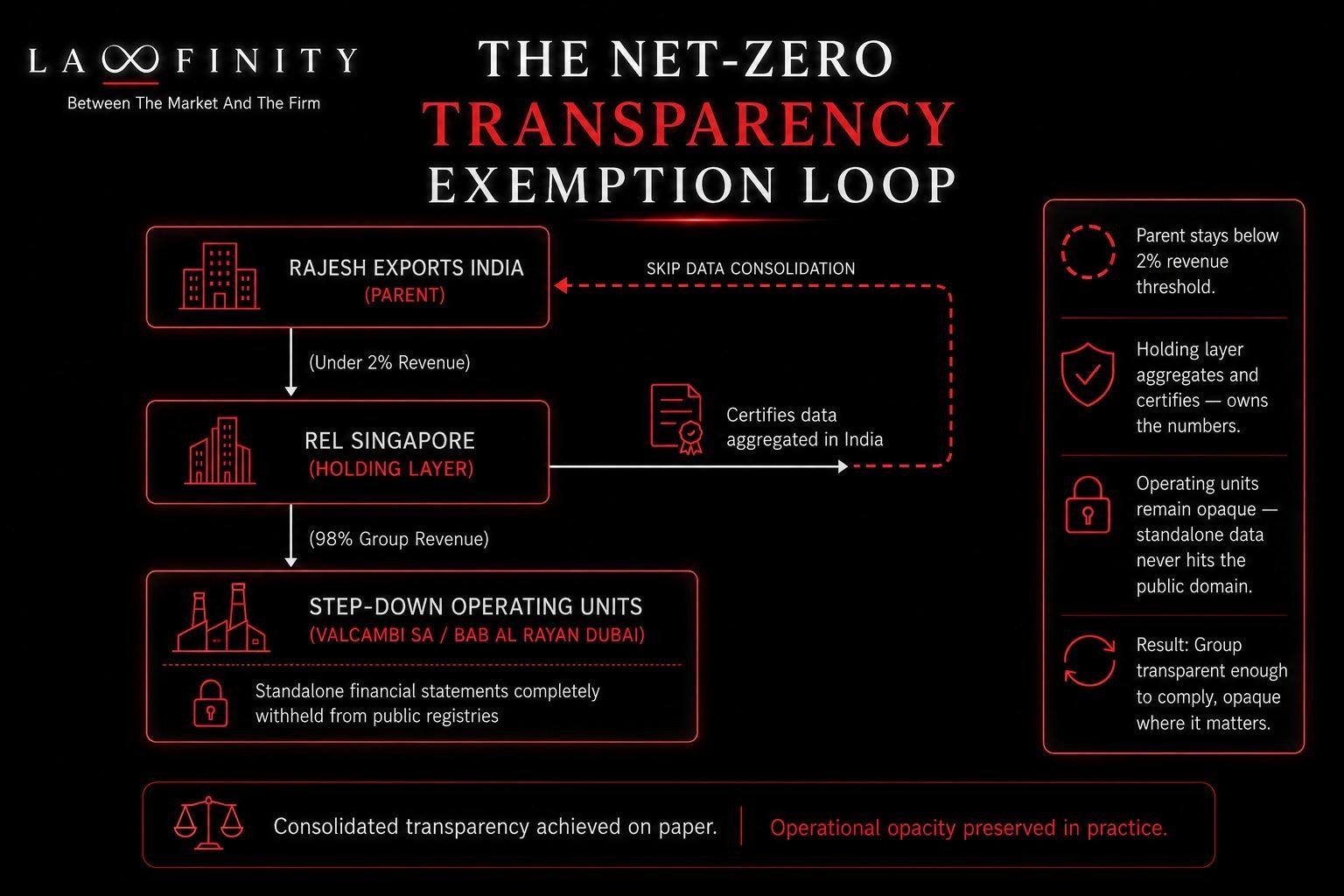

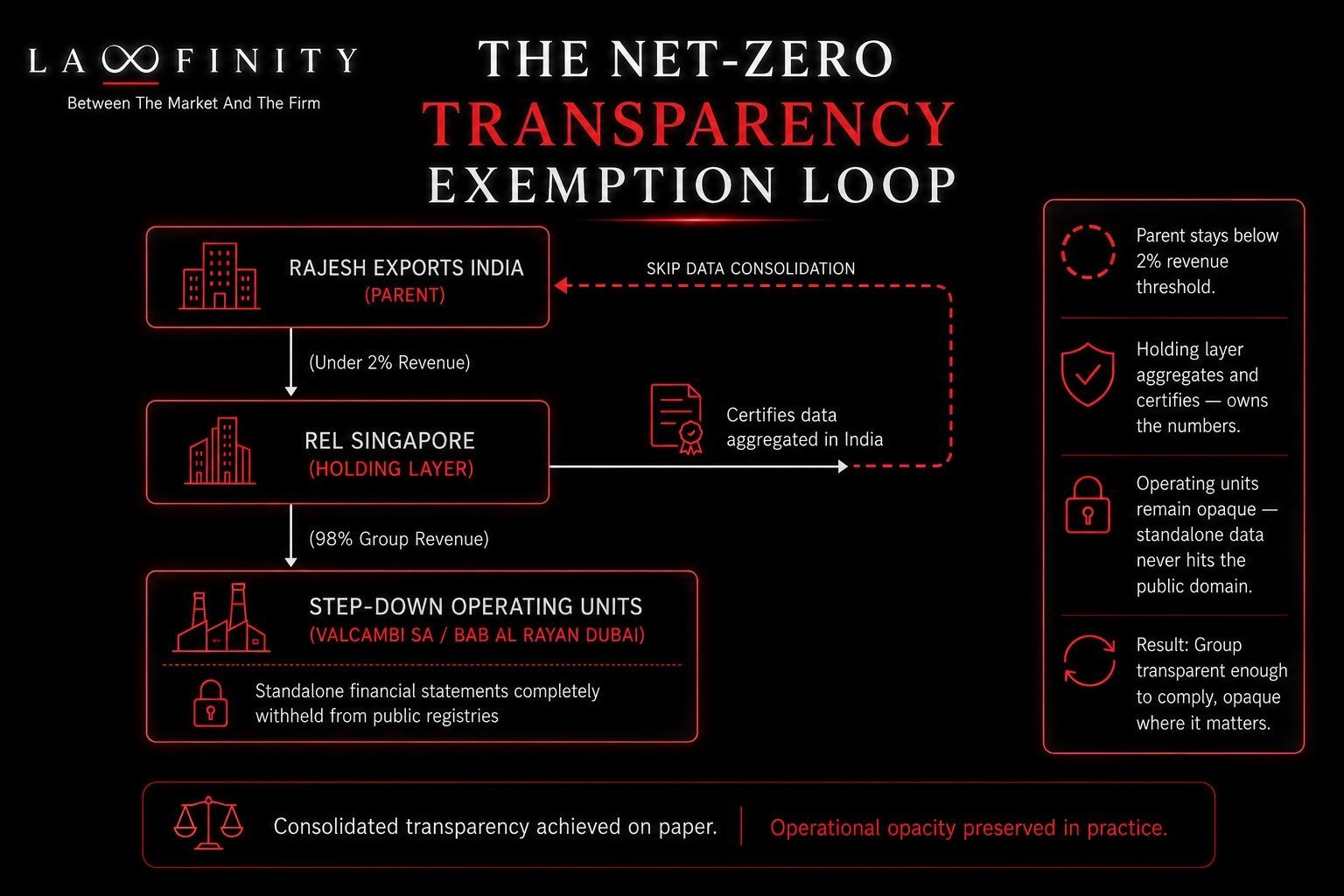

The regulatory findings unmasked an elaborate, multi-tier offshore holding chain spanning an Indian listed parent, an unlisted Singapore vehicle, an unaudited Swiss holding entity, the Valcambi refinery, and a Gulf jewelry affiliate. SEBI’s forensic audit alleges that a staggering 99.8% of the group’s reported consolidated revenue amounting to INR 15.15 lakh crore between FY21 and FY25, was materially misrepresented and artificially inflated through non-genuine accounting entries.

When the recovery question is mapped against this exact structure, one fundamental fact governs the commercial outcome: the structural maze that the regulator struggled to see through is the exact architecture a creditor must now recover through. The disclosure failure and the recoverability problem are two sides of the same coin.

The available value in this debt does not sit within India’s standalone borders, which generated less than 2 per cent of the group’s consolidated turnover. It sits behind the shifting cross-border corporate exemptions that, on the order’s account, created an artificial net-zero transparency loop in the first place.

According to SEBI’s findings, to secure local filing exemptions the Singapore arm certified to regional regulators that all financial aggregation would occur at the parent level in India, while the Indian parent treated the step-down records as insulated cross-border operations. It kept standalone financial statements for the core Swiss and Dubai revenue drivers withheld from public registries on both sides.

Multi-jurisdictional Litigation Strategies

This structural fragmentation completely redefines the nature of the mandate. A buyer of this non-performing exposure does not inherit a domestic enforcement file with an offshore footnote. It inherits an offshore recovery campaign with an Indian originating event.

Reaching real value requires a coordinated, multi-jurisdictional litigation strategy: securing Worldwide Freezing Orders (WFOs) out of the English High Court or Singapore High Court, deploying Norwich Pharmacal bank-disclosure orders to surface hidden asset migrations, and engaging Swiss investigative counsel to force data-access overrides against the unlisted operating layers. Each leg is a distinct cross-border corridor: the India-UK route through the English courts, the India-Singapore legal corridor at the holding layer, the India-UAE leg into the Gulf, and the mandate forms where they meet. Domestic recovery practices field the local enforcement cleanly, but the international asset-tracing track not at all.

This is where traditional distressed-debt screening metrics fail. Special-situations funds routinely evaluate Indian corporate distress by sector, underlying domestic security, and bank discount. None of these lenses measures the single variable that decides the financial outcome here: whether the offshore assets can be reached behind the corporate veil.

A corporate guarantee is worth only the clean provenance of the wealth standing behind it. The subcontinental debt worth buying is the debt with a reachable offshore asset base. But that is a different list from the auction notices the banks are publishing. Treating the two as identical is the difference between buying an asset recovery and buying a stranded lawsuit.

Law Firms Positioned for the Work

Read as a question of cross-border mandate formation: who actually gets instructed on work like this, and how the instruction reaches them. The competitive landscape of the India corridor looks nothing like the league tables. The legal institutions positioned to drive this cycle are not the standard corporate India desks.

The mandates belong to the specialised partner benches built along the exact route the capital takes: the London civil-fraud practices that run international injunctive tracing, the Singapore disputes teams sitting at the intermediate-holding layer, and the continental white-collar specialists managing the data-access parameters. This multi-disciplinary capability exists globally in fragmented pieces; what remains rare is the firm that has assembled the corridor end-to-end.

The category this development points to is not standard domestic insolvency or IBC-driven recovery, which is crowded, nor local asset recovery, which Indian law firms own. It is the narrow, highly lucrative band where the two intersect: cross-border debt enforcement against Indian corporate groups whose realisable value has been structured offshore. A buyer who can forensically read which exposures rest on an attachable asset base, and a firm that can run the recovery through the entire length of the transnational pipeline, are positioned for work the market will consistently misprice:

– the auction-list buyer overpaying for corporate value it cannot reach;

– the domestic recovery firm winning a local judgment it can never satisfy.

For a foreign firm, this is the real shape of India market entry through the corridor: not a desk and not an alliance, but the capability to read where the work forms and to be built along the route before it arrives. That is the line between an India strategy and an India brochure.

All references to the SEBI matter and the underlying group structure above are to allegations in an unadjudicated interim order. The company has denied wrongdoing and retains the right to respond.

Lawfinity Solutions advises international law firms on cross-border legal market positioning. If the India corridor is a live question for your firm, we would be interested in a conversation. Lawfinity works with one firm per jurisdiction. Engagements begin with a single conversation about your firm’s current position and where the corridor question is live for you. Write to Prachi Shrivastava