The Flashpoint

On 3 June 2026, SEBI issued a 109-page interim ex-parte order against Rajesh Exports and its promoter-chairman, alleging that approximately INR 15.15 lakh crore ( $16.3m) which is about 99.8% of the revenue the company attributed to its subsidiaries between FY21 and FY25, was misrepresented. SEBI’s probe exposes a distinct jurisdictional trap: the regulator alleges the inflated revenue was parked entirely in an unaudited Swiss holding company directly above the Valcambi refinery. When forensic auditors moved in, the company successfully stalled the investigation by using Swiss data-protection laws as a shield to withhold all subsidiary records.

(All references below are to allegations in an unadjudicated interim order. The company has denied wrongdoing and retains the right to respond.)

The Anatomy of the Offshore Corporate Chain

The regulatory probe maps a multi-tiered corporate architecture designed to isolate operations from domestic oversight. As detailed in the SEBI Interim Order, the fund and asset flow structures across five distinct layers:

Indian Listed Parent ➡️ REL Singapore (Holding) ➡️ Global Gold Refineries AG (Unaudited Swiss Holding) ➡️ Valcambi SA (Swiss Operating Refinery) ➡️ Valcambi USA (Dormant)

(Note: This chain operates alongside Bab Al Rayan, a synchronized Gulf-based group entity.)

The Multi-Corridor Practice Matrix

This structural configuration instantly lights up four distinct cross-border corridors, converting a localised regulatory inquiry into a highly complex, multi-jurisdictional dispute ecosystem:

● India-Switzerland (The Flashpoint): This is the highest-value corridor. It houses the physical operating assets, the critical subsidiary accounts, and the primary battleground over foreign data-protection and corporate secrecy shields.

● India-Singapore (The Consolidation Layer): Historically the holding jurisdiction of choice for outbound Indian capital, Singapore is exposed here as the exact layer where consolidated financial visibility fractures, driving immediate demand for corporate restructuring and forensic diagnostics.

● India-UAE & India-US (The Asset-Tracing Routes): These secondary corridors are triggered immediately for parallel asset-tracing mandates, cross-border fund-flow analysis, and international recovery strategies targeting downstream group assets.

–

Sector heat: gold, precious metals and commodities trading will be impacted first. But the transmissible risk reaches every India-listed group that books material revenue through offshore holding chains such as pharma, IT services, renewables, EPC/infrastructure, and family-controlled conglomerates running Singapore, Swiss, Dutch or Mauritius holdcos. The order effectively reprices the legal risk of the offshore holding structure itself.

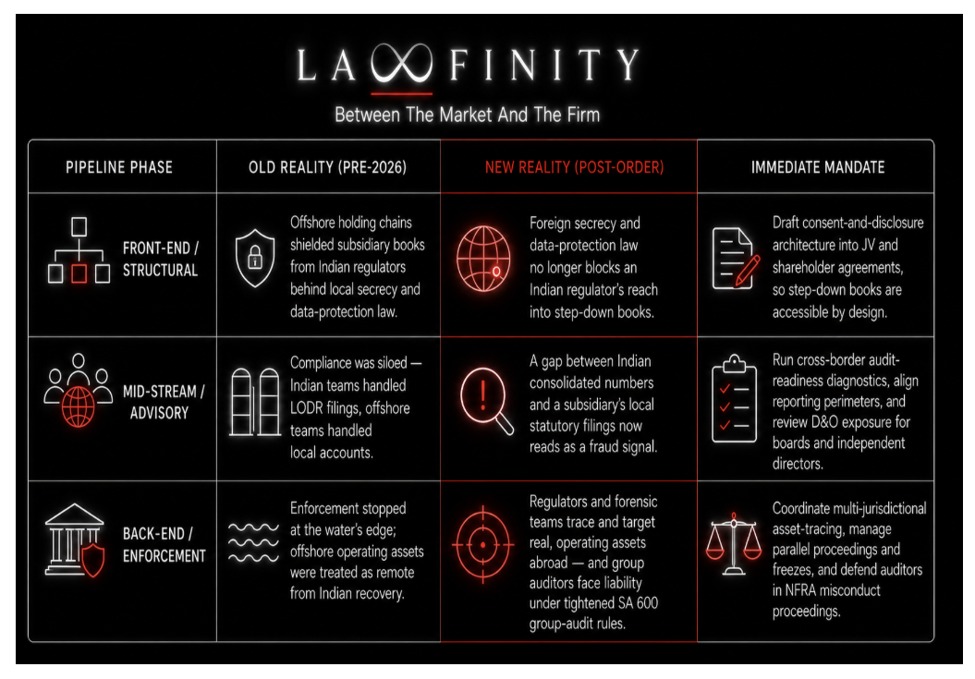

The Mandate Pipeline Matrix

The old assumption no longer holds if we speak of an offshore subsidiary’s books being treated as a black box, safe from Indian scrutiny. SEBI rejected the Swiss data-protection defence and set the group’s trillion-rupee revenue claims against Valcambi’s own audited standalone accounts, which ran to only a few hundred crore Rupees a year. Read alongside NFRA’s move to tighten the group auditor’s responsibility for component auditors under a revised SA 600, the offshore holding chain is now a live disclosure and enforcement surface. That reallocates work across the whole pipeline:

Competitive Playbook for Foreign Firms

The opening here is not generic securities litigation – Indian firms own that. It is the cross-border layer domestic practices cannot reach cleanly: the evidence, the operating assets and the secrecy defences all sit abroad.

The raw capability is already assembling around the corridor. Since the BCI’s 2025 amended rules, foreign firms have circled India through offshore desks rather than wait on registration – Child & Child paired with Mumbai’s Solicis Lex, RPC built a Singapore-based India desk, and US firms such as Mandelbaum Barrett launched their own. Full-spectrum India practices now describe themselves as spanning transactions, disputes and regulatory work across Singapore, London and New York at once, as Sidley characterised its India practice in early 2026. London carries India-focused civil-fraud and asset-recovery benches that clients already cite (among them Penningtons Manches Cooper’s India group), Singapore offers deep India restructuring-and-disputes capability, and GIFT City is being built out as an India-seated dispute venue.

What almost none of that was built for is the inverse problem this order creates. The offshore India desk, the capital-markets bench and the arbitration practice are all oriented toward inbound work.

The Rajesh Exports pipeline runs outbound: an Indian-listed parent, an operating asset and audited accounts in Switzerland, an intermediate holding layer in Singapore, and a foreign-secrecy defence, all of which must be tied back to a SEBI and NFRA process in India. Capturing it takes three things assembled into a single stack:

– Geneva/Zurich evidence reach;

– Singapore holding-company coordination; and

– an India-regulator-facing narrative.

Most firms hold one or two of those pieces and treat the offshore subsidiary as someone else’s audit problem; very few have deliberately built the combination.

That is the gap.

The profiles closest to closing it

– the full-spectrum India practice already running disputes and regulatory work across three financial centres, which can extend into outbound forensic coordination;

– the Geneva or Zurich investigations bench sitting on the data-protection question, the moment it has an India-facing channel;

– the Singapore disputes practice positioned exactly at the intermediate-holding-company layer; and

– the forensic-led boutique that can productise a fixed-scope “disclosure-perimeter review” before the elite firms package it.

The Strategic Signal

Lawfinity’s Insight: The winnable category here is two-sided and sequential.

1. First, the preventive mandate: every India-listed group with an offshore holding chain now needs a structural review proving its disclosure perimeter and audit-access would survive a SEBI inquiry.

2. Second, the remedial mandate: when a structure fails, the coordinated cross-border investigation and offshore asset-tracing capability that domestic firms cannot field alone.

A foreign firm that wants either should stop marketing a generic “India Desk” and instead stand up a named Cross-Border Audit-Access & Disclosure-Perimeter offering, anchor it with thought leadership on the Switzerland-vs-Indian-regulator question, and secure Swiss-Singapore-India lateral or best-friends coverage now while the category is still being defined and before the final order makes it crowded.

Sources: SEBI interim order dated 3 June 2026 and contemporaneous reporting. All matters described are allegations in an interim, unadjudicated order; the company and its promoter have denied wrongdoing and retain the right to respond.

Lawfinity Solutions advises international law firms on cross-border legal market positioning. If the India corridor is a live question for your firm,we would be interested in a conversation. Lawfinity works with one firm per jurisdiction. Engagements begin with a single conversation about your firm’s current position and where the corridor question is live for you. Write to Prachi Shrivastava