A Lawfinity note on dead letter assets, sovereign overhang, and where the next mandates are forming

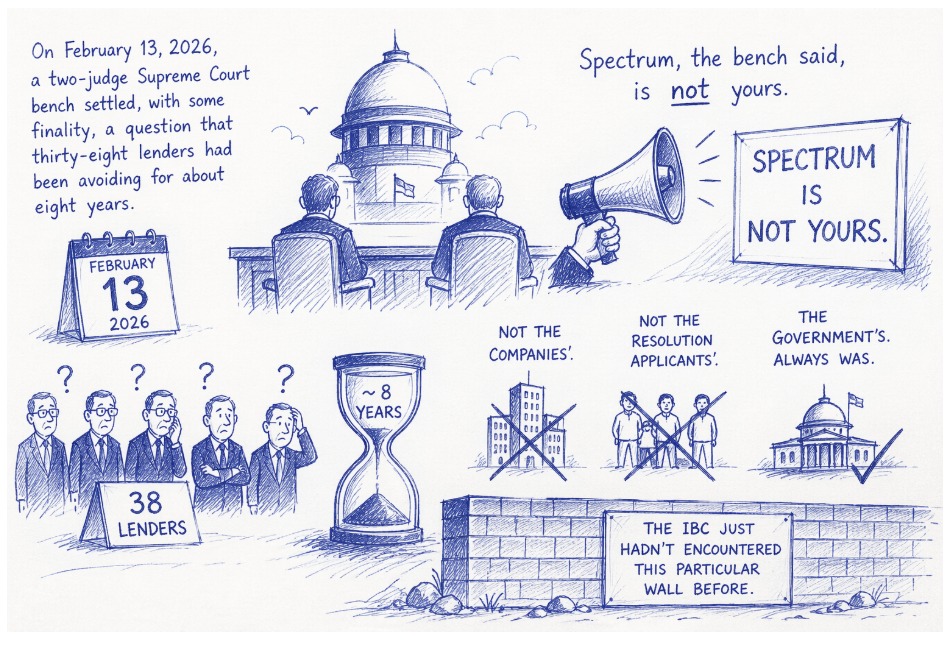

Spectrum, the bench said, is not yours.

Not the companies’. Not the resolution applicants’. The government. Always was. The IBC just hadn’t encountered this particular wall before.

All of it built on an asset that turned out to be a dead letter asset – something that sits credibly on a balance sheet, anchors a credit decision, and becomes unrecoverable precisely at the moment you need to recover it.

This is not a story about bad lawyering. The lenders’ assumption was commercially rational, and institutionally consistent. No one was questioning it, is what is even more interesting.

Spectrum belongs to a category of assets we’ve been thinking about as carrying sovereign overhang – the condition where a government-retained resource casts a legal shadow over what looks, commercially, like a private arrangement. Mining concessions carry it. Port and PPP concessions carry it. Broadcasting licences carry it. Vodafone Idea, with ₹1.87 lakh crore in debt and an NCLT insolvency warning already on record, is about to discover whether its spectrum does too.

The shadow was always there. It just wasn’t visible from where the lenders were standing when they wrote the cheques.

INDIA-CROSS BORDER LEGAL MARKET

India has not signed a single bilateral insolvency recognition treaty. Not one, in ten years of IBC. Which means when a Singapore-incorporated holding company or a Mauritius-structured PE fund participates in an Indian resolution process and finds that the rights it thought it acquired cannot be exercised – there is no formal framework for what happens next.

What there is, is a treaty.

In PCA Case 2013-09, Mauritius-incorporated investors went to the Permanent Court of Arbitration after India cancelled spectrum-linked satellite licences. The tribunal found India guilty of expropriation and breach of fair and equitable treatment. The domestic route – NCLT, NCLAT, Supreme Court – produced zero recovery. The treaty route produced an award against the Republic of India.

So we know that to this extent, it already happened.

“The disputes that will travel this corridor are being shaped now.” |

This is the part that the spectrum ruling makes newly visible: a jurisdictional corridor is forming, in real time, for foreign investors holding India-linked regulated-sector positions through offshore structures. The precise corridor strength is in the ability to answer for the gap between what Indian tribunals can approve and what they cannot actually transfer. The domain strength is also in the treaty architecture that offshore investment structures have been sitting on all along.

The disputes that will travel this corridor are being shaped now. In financing documents already signed, resolution plans are negotiated as we write this and also in the question of whether a Mauritius or Singapore holdco’s investment qualifies for BIT protection when the asset underneath it turns out to be sovereign.

The practitioners who will be well-positioned for those mandates are the ones reading that gap now, before it becomes a filing. Have you watched the Lawfinity Intelligence Briefs report on this corridor?

This is the kind of upstream signal we track. More to follow.

Lawfinity Solutions works with law firms and practitioners on India cross-border legal market positioning and intelligence.