By Prachi Shrivastava, Founding Advisor, Lawfinity Solutions

A vendor has run its sales motion several hundred times. A mid-market or boutique buyer runs a serious legal-technology purchase once every few years. The vendor therefore enters the process with far more experience than the buyer.

For the global boutique or mid-tier firm, this asymmetry carries a punishing financial sting. In a mega-firm, a dedicated Legal Ops department with an independent budget buffers the blow. In a mid-market or boutique firm, whether navigating the high-stakes corridors of London and New York or the breakneck growth of Mumbai and Delhi, the buyers are the fee-earners.

When a five-partner tech committee spends twelve hours sitting through vendor pitches, evaluating RFPs, and attending debriefs, the firm isn’t just investing administrative time. At an average mid-market partner rate of $750 per hour, that committee has just burned $45,000 in unbilled opportunity cost before ever seeing a software contract. While the vendor invests paid corporate capital to sell to you, your firm is draining its own equity pool. You are losing margin before you have even seen the quote.

Worse, almost everyone positioned to help you narrow this asymmetry is themselves inside the market: the vendor sells, the analyst ranks within the categories the vendors fund, the integrator implements what it is certified in. Each can provide valuable input, but none approaches the decision from a completely neutral position.

What follows is the same market read from outside it, by someone with nothing in any category and no seller behind the words. None of it is secret. All of it is easier to see when your primary metric is year-end partner distributions rather than software market share.

The map you were handed is already out of date

The traditional software categories: research, drafting, CLM, litigation review, the ubiquitous “AI assistant”, are converging faster than any law firm procurement cycle can move. Research tools have added drafting; contract tools have added review; nearly everything has bolted on a generative AI wrapper. By the time a “category leader” list is published, the leaders are competing outside the box it sorted them into.

We see this play out when a managing partner spends six months building a complex, color-coded spreadsheet to compare three distinct point solutions for contract automation, only to discover that a legacy research giant has just acquired a boutique litigation-tech startup, rewriting the functional boundaries of the software overnight.

Organize a technology search around last year’s map, and you are shopping for a market that no longer exists in that shape. For a mid-market firm where technology budgets typically hover around 3% to 5% of gross revenues, spending $50,000 on a point solution that becomes redundant or obsolete within nine months isn’t just an IT oversight, it is capital deployment that fails to yield a return before the technology shifts beneath your feet.

Feature presence is not feature maturity

A great many “AI” capabilities exist because the venture capital cycle demanded an AI story, not because a law firm’s actual client work pulled them into being.

Many vendors added AI features because investors expected them to, not because clients were asking for them. The consequence is a structural gap between what demos cleanly on a pristine sample document and what survives contact with a messy, real-world matter and a skeptical partner.

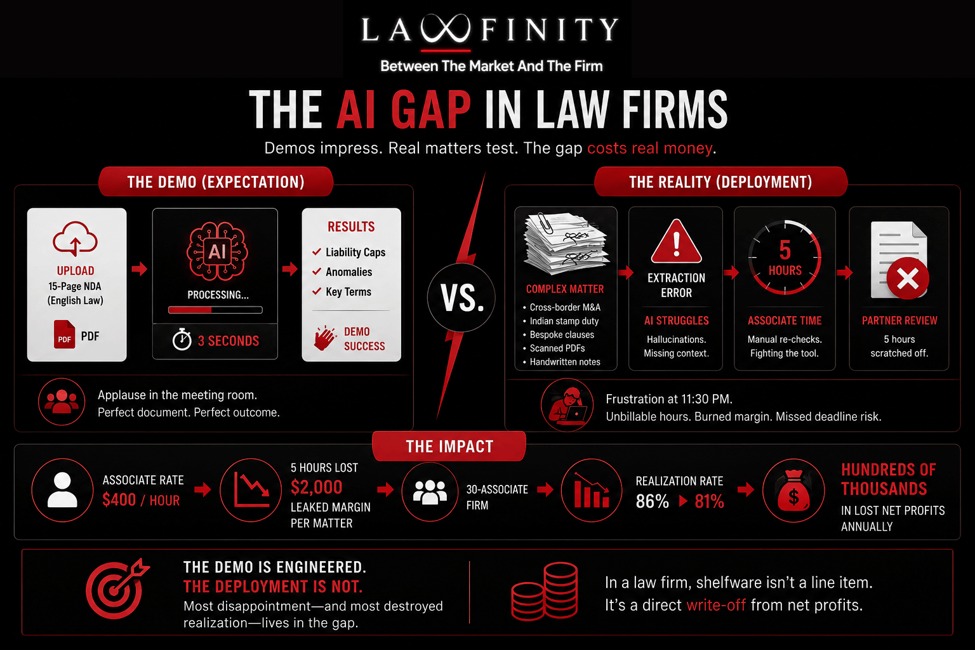

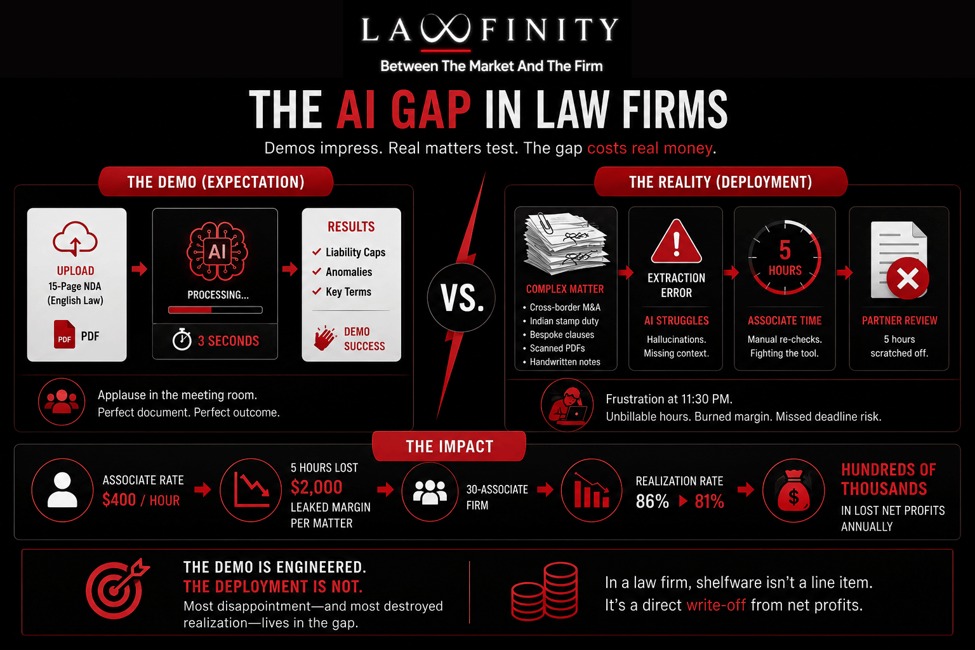

Consider the typical Tuesday afternoon Zoom demo: the sales representative uploads a perfectly formatted, 15-page, English-law NDA. The AI extracts the liability caps and anomalies in three seconds flat, and the room applauds.

But transition to a Saturday night at 11:30 PM, where a senior associate is working on a cross-border M&A transaction involving a tangled web of Indian stamp duty nuances, bespoke indemnity clauses drafted by a hostile counterparty, and scanned PDFs with handwritten annotations. The software throws a silent extraction error or hallucinates a clause. The associate then spends five unbillable hours manually re-checking the machine’s work, fighting a clunky UI while a critical deadline looms.

On Monday morning, the partner looks at the pre-bill, sees the associate’s inflated time, and promptly scratches those five hours off to keep the client happy. At an associate rate of $400 per hour, that is $2,000 in leaked margin on a single matter.

When this happens across a 30-associate firm, realization rates drop from a healthy 86% down to 81%, translating to hundreds of thousands of dollars in lost net profits annually. A product can perform well in a demo and still create problems in day-to-day legal work. Those problems are where firms lose time, efficiency and margin. In a law firm, shelfware isn’t an abstract accounting line item; it is a direct write-off that comes straight out of net cash profits.

The pricing is opaque on purpose

No two vendors price the same way: per seat, per matter, per data volume, per use, per “value,” per some bespoke unit invented for the quote sitting in front of you. Non-comparable pricing is a deliberate design feature: when every vendor measures value differently, comparing prices becomes far more complicated than comparing features. The harder it is for a firm to lay two offers side by side, the more the conversation stays on the flashy features of the demo and off the reality of the ledger.

Vendors frequently exploit this by dangling the carrot of the “disbursement mirage.” They pitch a pricing model that looks like it maps cleanly to individual matters, say, charging $120 per automated contract generation, convincing the tech committee that this cost can be passed directly through to the client as a technology fee.

The illusion shatters six months later when a sophisticated corporate client reviews your invoice against their strict Outside Counsel Guidelines (OCGs). Today, corporate legal departments reject technology surcharges up to 78% of the time. The client flatly states, “We pay you for legal expertise, not your software overhead.” The disbursement is written off, and that opaque cost lands squarely back on the firm’s overhead ledger, eating directly into partner equity. A buyer who cannot accurately compare price is negotiating with one hand tied behind their back, which is precisely the point.

The reference signals are mostly theatre

The logo wall, the “trusted by,” the marquee global firm listed at the top of the website—these are marketing artifacts, and they are highly gameable. The signals that would tell a boutique or mid-market buyer something useful are the ones never published on the website: net renewal rates, how many seats are actually active twelve months after implementation, and how many deployments quietly lapse at the eighteen-month mark.

Behind that prestigious boutique logo prominently displayed on a vendor’s homepage is a hollow institutional reality: one tech-forward partner at that firm bought three licenses using a discretionary marketing budget, used it twice, and forgot to cancel the subscription. Meanwhile, the remaining ninety fee-earners at the firm continue to draft documents using pure grit, historical Microsoft Word templates, and manual proofreading.

An independent audit of legal tech deployments frequently reveals that while a firm pays for a 100-user enterprise license, active daily usage drops below 12% past month six. Vendors often highlight deployments. Buyers should focus on sustained usage, because that is a better indicator of whether the product is delivering value in practice.

You are buying into a market about to consolidate

A field this crowded, funded on this much near-identical venture capital, does not stay this crowded. Some of what is sold confidently today will not have a vendor behind it in twenty-four months. That makes vendor durability a critical part of the purchase strategy. You are betting on which software firms will survive the inevitable macroeconomic shakeout, not just which tool has the slickest user interface.

When a legal-tech startup goes under or gets acquired and cannibalized by a legacy conglomerate, the true loss to a mid-market firm isn’t the unrecovered software licensing fee. It is the invisible, structural friction that follows.

If your active matter data is locked inside a dying platform, it requires an expensive, urgent manual migration. Worse, it triggers the billable-hour-destroying cost of having to drag a busy partnership through the painful process of learning an entirely new system all over again.

When you account for the lost productivity, tech retraining typically costs a firm an average of $10,000 per fee-earner in lost billable capacity, yet no pitch has ever included the possibility of its own disappearance.

The read with no seller behind it

None of this analysis requires inside information. It requires only a structural positioning that almost no one advising a legal-technology buyer occupies: standing entirely outside every product category, paid by no vendor, and wholly indifferent to which specific tool wins the mandate.

Each party a law firm buyer would naturally turn to for guidance is paid for the buyer to arrive at a particular destination. The consultant who is certified in a specific platform wants you to buy that platform; the vendor analyst wants you to buy within the matrix they have built.

The reading of the market that owes absolutely nothing to any of them is the scarce one. This isn’t because it is inherently cleverer, but because almost no one in the legal-tech ecosystem is standing where it can be done, completely outside the transaction, focused exclusively on the firm’s net margins, realization rates, and long-term equity value.