A Kerala High Court ruling on 1 June restated what lawyers structuring India joint ventures already know: that shareholder deadlocks and the division of company assets fall within the exclusive jurisdiction of India’s National Company Law Tribunal (NCLT) under Chapter XVI (Sections 241 and 242) of the Indian Companies Act, 2013, which governs statutory shareholder remedies for mismanagement and unfair prejudice. These corporate divorces cannot be arbitrated. It is settled law; the position has held since Haryana Telecom and was locked by the four-fold test in Vidya Drolia. No one structuring these ventures was surprised on 1 June.

What is worth saying is what that settled position costs, and who is placed to be paid for it.

Billable Mismatch

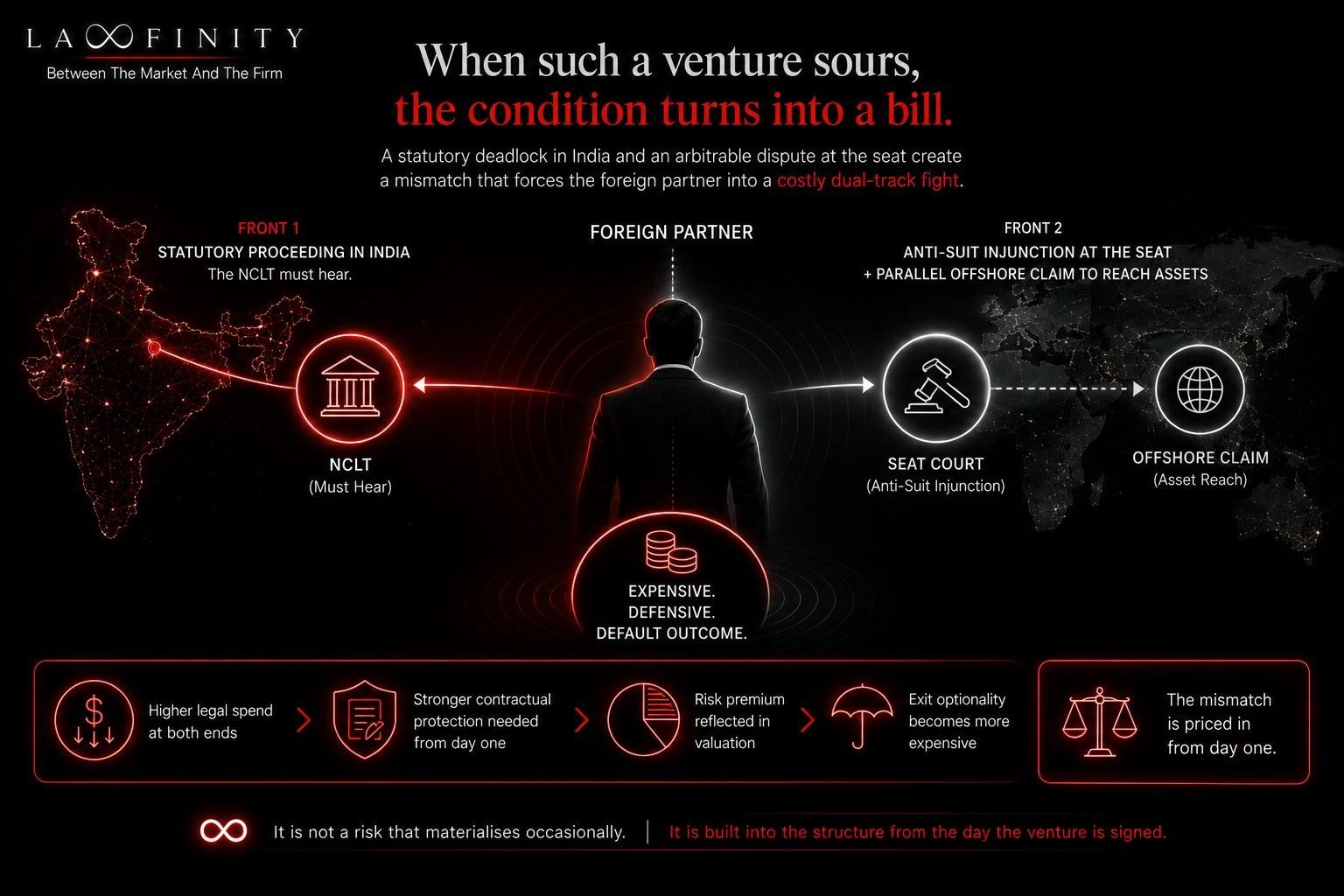

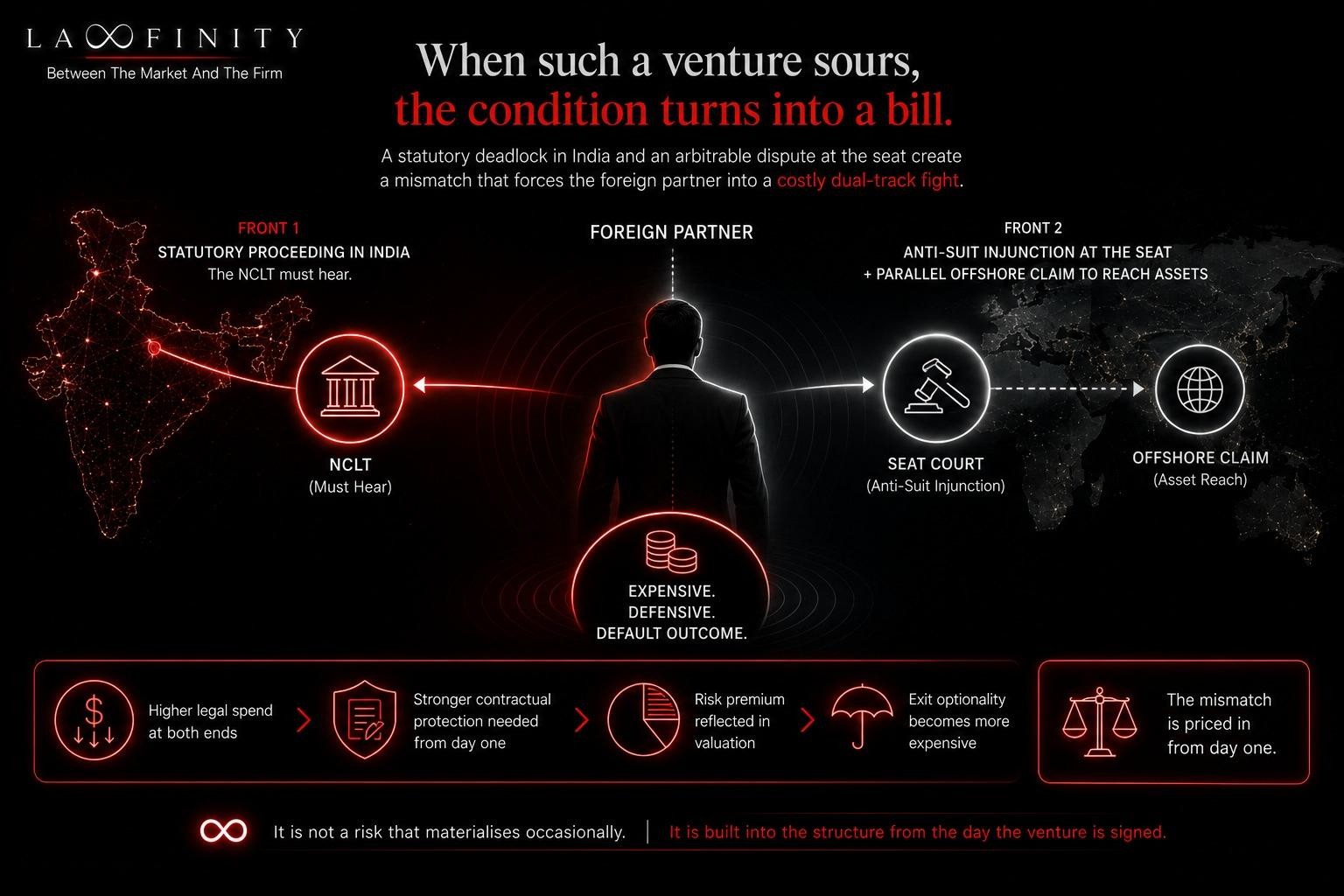

The cost comes from a mismatch: India treats a corporate deadlock as an in rem statutory matter for its tribunal. The seats a foreign partner chooses for the venture (overwhelmingly London and Singapore) treat the same deadlock as a private, arbitrable dispute: There’s Fulham v Richards in England, and the position the Singapore Court of Appeal enforced in Anupam Mittal v Westbridge, restraining an Indian founder by anti-suit injunction for taking an oppression claim to the NCLT in breach of a Singapore-seated clause. So the identical dispute is arbitrable at the seat and non-arbitrable in India. That divergence is a permanent condition that sits under every cross-border venture with an Indian operating company and a foreign seat.

When such a venture sours, the condition turns into a bill. The foreign partner cannot simply hold its seat: the Indian counterparty files in the NCLT, which the tribunal must hear, and the partner is forced to fight on two fronts at once:

1. defending the statutory proceeding in India while paying counsel at the seat for an anti-suit injunction; and often

2. a parallel claim offshore to reach assets, because an award good at the seat is hard to enforce against assets sitting in India.

The dual-track war is expensive, defensive, and the default outcome of the mismatch. It is not a risk that materialises occasionally; it is priced into the structure from the day the venture is signed even if everyone forgot to literally price it.

The Commercial Question

The mandate pipeline does not go to the firm with the fastest reaction. Reaction is available to everyone: the anti-suit is a reactive remedy, triggered by the filing, and any competent firm can run it. Also, international firms work with Indian counsel who watch the registries on the ground. But that reactive and narrow intelligence that:

– surfaces matters once they are filed;

– only for the ventures that counsel already acts in;and

– which travels on the Indian firm’s own commercial terms.

is a case feed, not a map.

What decides who is paid is positioning, set before the dispute. The firm that does well out of the mismatch is the one already in front of the foreign partner:

– at the structuring stage, where the seat, the security and the exit can be built to blunt the dual-track exposure; and

– in the relationship, so that when the venture breaks it is retained rather than considered.

Being in that position is not a function of reacting faster, or of an Indian correspondent’s alert. It is a function of knowing, across the corridor, which ventures and which sectors carry this latent exposure, and which foreign investors are sitting on it unpriced. A forward, market-level view needs to be taken and I wouldn’t blame the counsel on both sides of the border for neglecting it. It is not their job.

The Kerala ruling changed nothing about the law. What it should change is where a firm looks for the work the mismatch produces: not at the filing, where everyone arrives at once and competes on reaction, but in the positioning done long before it. It pays for itself to be the firm already trusted by the foreign partners whose ventures sit on this exposure, and knowing, across the corridor, which ventures those are.

Lawfinity Solutions advises international law firms on cross-border legal market positioning. If the India corridor is a live question for your firm,we would be interested in a conversation. Lawfinity works with one firm per jurisdiction. Engagements begin with a single conversation about your firm’s current position and where the corridor question is live for you. Write to Prachi Shrivastava