Bright lines invite structuring. That is a neutral observation about how legal frameworks behave: where a clear threshold is drawn, commercial engineering concentrates around it.

India’s listing framework draws such lines for related-party transactions. Under the SEBI LODR Regulations, a related-party transaction above a materiality threshold (broadly, INR 1,000 crore or ten per cent of consolidated annual turnover, whichever is lower) must be put to a vote of public shareholders. Beneath that sits a second and, for present purposes, more consequential line: the definition of who counts as a “related party” at all. The first line is about value; the second is about characterisation. Engineering concentrates on the second, because a transaction that falls outside the definition never reaches the gate in the first place.

The question for cross-border counsel is not whether this happens. It is where it concentrates, and what forms downstream of it.

A public illustration

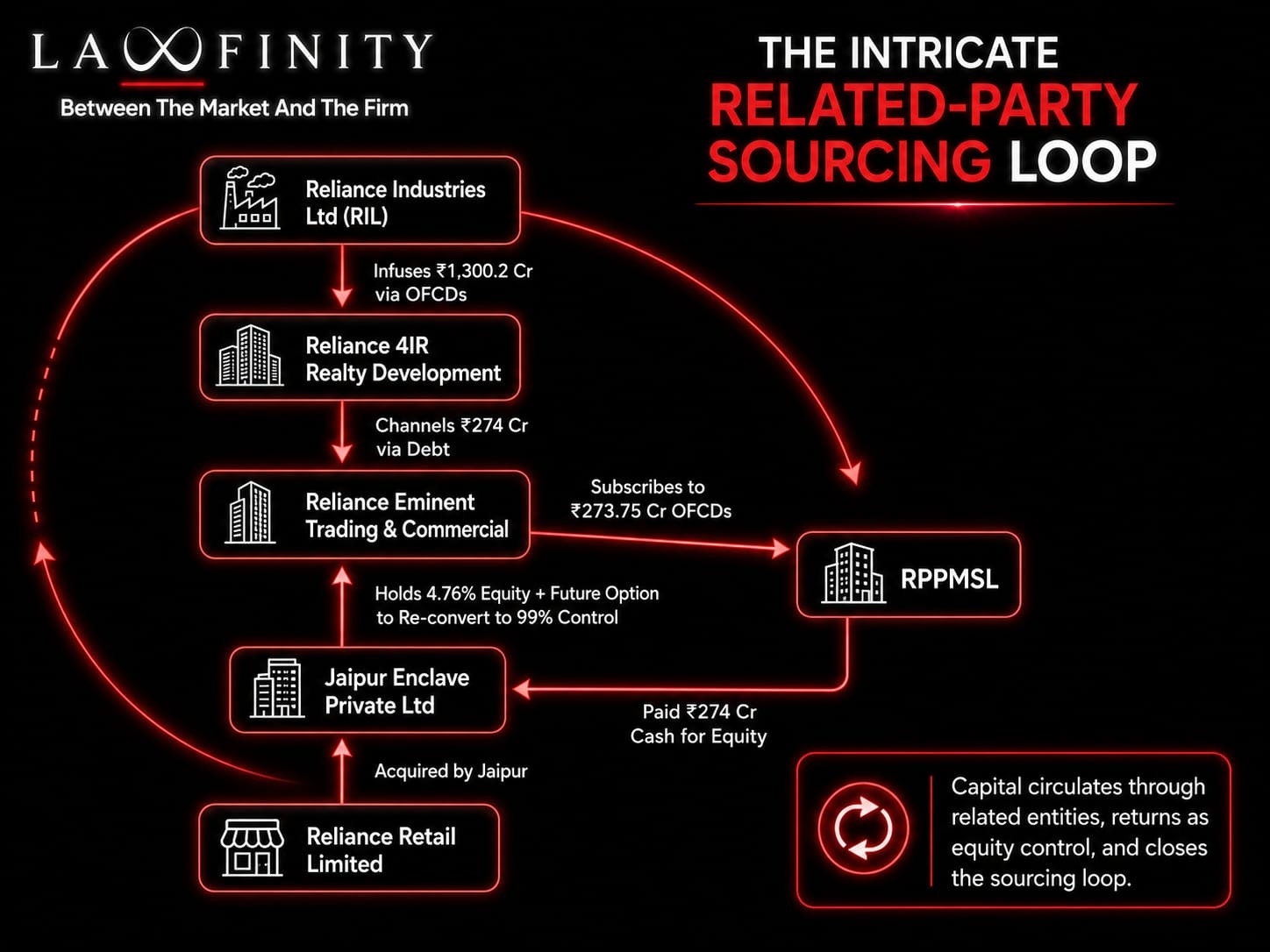

The clearest current illustration is one the company itself disclosed. On 13 April 2026, Reliance Retail sold its entire stake in Reliance Projects & Property Management Services Ltd (RPPMSL) to Jaipur Enclave Private Ltd for INR 274 crore; Reliance’s filing records its position that the buyer is not part of the promoter group and that the transaction is not a related-party transaction.

What drew governance commentary was the shape around it, as reported by Mint. A unit that earned INR 379 crore on roughly INR 9,323 crore of revenue in FY25 was sold for INR 274 crore to a company with effectively no revenue of its own. Shortly afterward, that buyer issued some INR 273.75 crore of optionally convertible debentures to a Reliance step-down entity, Reliance Eminent Trading, close to the purchase price with the feature that, on conversion, Reliance Eminent’s stake would cross ninety-nine per cent and the unit would return to the group.

Mint reported that it could not confirm whether the buyer then used that sum to pay Reliance Retail. Reliance maintains the transaction was at arm’s length.

The point is not to adjudicate it; that belongs before the regulator. Reliance’s position is on the record, and governance specialists have argued that a circular, net-zero structure of this kind cannot fairly be read in isolation and engages the anti-abuse provisions of the listing framework. The feature worth isolating is structural, and larger than any single transaction: a convertible instrument turns relatedness into a question of timing. A counterparty unrelated on paper today can become a controlling one tomorrow, on conversion.

The zone, not the deal

What makes this a zone rather than a single deal: the live question is rarely whether a transaction is large enough to need a shareholder vote; it is whether the counterparty is “related” at all, and whether the deal can be read on its own.

A convertible instrument lets a group keep both answers open. The buyer is unrelated today but if the group can convert its debentures into a controlling stake whenever it chooses, “related” becomes a switch it holds rather than a fixed fact. And when the cash that funds the purchase travels in a loop, out of the group and back into it, the asset changes hands on paper without an outside buyer ever putting its own capital at risk.

That the listing rules carry anti-abuse provisions at all is the regulator’s own admission that this can be done, that the boundary of “related” can be built around. And it is a feature of the system, not of one company: related-party transactions across India’s largest listed firms run, by the available measures, into the trillions of rupees a year. The same definitional questions sit beneath all of them.

The Singapore layer

The same divergence between substance and visible form widens when a group routes its intermediate holding structures through a jurisdiction such as Singapore, frequently for ordinary reasons of investment and asset protection.

Many jurisdictions, Singapore among them, allow an intermediate holding company to be exempted from preparing and filing its own consolidated financial statements where consolidation is carried out higher up the group. That is a legitimate and common position. Its structural consequence, for an outside observer, is that the economic substance of the layers beneath an intermediate holding company may not be fully visible in the jurisdiction where that company sits. It is captured, if at all, only at the level of an ultimate parent in another country. Relatedness and value can be made less visible by characterisation at home; substance can be made less visible by location abroad. The two compound.

Where it meets the corridor

A structure engineered around a domestic or regional boundary does not stay local once someone pulls on it. The instruments that absorb the relatedness or distribute the substance (convertible debentures, intermediate and offshore holding layers, consideration that moves in a loop) are the features that carry a dispute across borders when a minority shareholder, an institutional investor or a regulator challenges it.

The route is, by now, familiar to anyone who works the corridor. A cross-border joint venture is typically anchored by an English- or Singapore-law shareholders’ agreement, so a deadlock or a contested transaction is, at the seat, a contractual matter which runs immediately into the tension with India’s statutory tribunal jurisdiction, where the same dispute is treated as non-arbitrable and where the local assets sit. From there it becomes what such disputes usually become: a contest over which forum governs, and an effort to follow value through the holding layers. The mechanics are not novel. What is worth noticing is where they originate.

The Durable Point

Each vantage point reads its own half well. The domestic governance analyst reads the listing question and, reasonably, stops at the border. The cross-border disputes practice tends to meet the matter only once it has already become an enforcement or activist action abroad. The connection between the two: the densest zone of domestic governance arbitrage is a leading indicator of where corridor disputes will later form. This is a corridor-level read, and it is the kind of read neither vantage point is positioned to produce on its own.

These particular matters will resolve as they resolve, and the point does not depend on how they do. What lasts is the shape they reveal. The convertible option that keeps a buyer “unrelated,” the consideration that leaves the group and returns to it, the holding company that sits one jurisdiction away from where its own substance is recorded. Each is drafted to solve a domestic problem, and each is the precise thing a claimant’s counsel later has to unwind when the structure is challenged. A dispute of this kind is not born when the freezing order is sought in London; it is born years earlier, in the structuring, before it has a name. It surfaces in London. It is made in India.