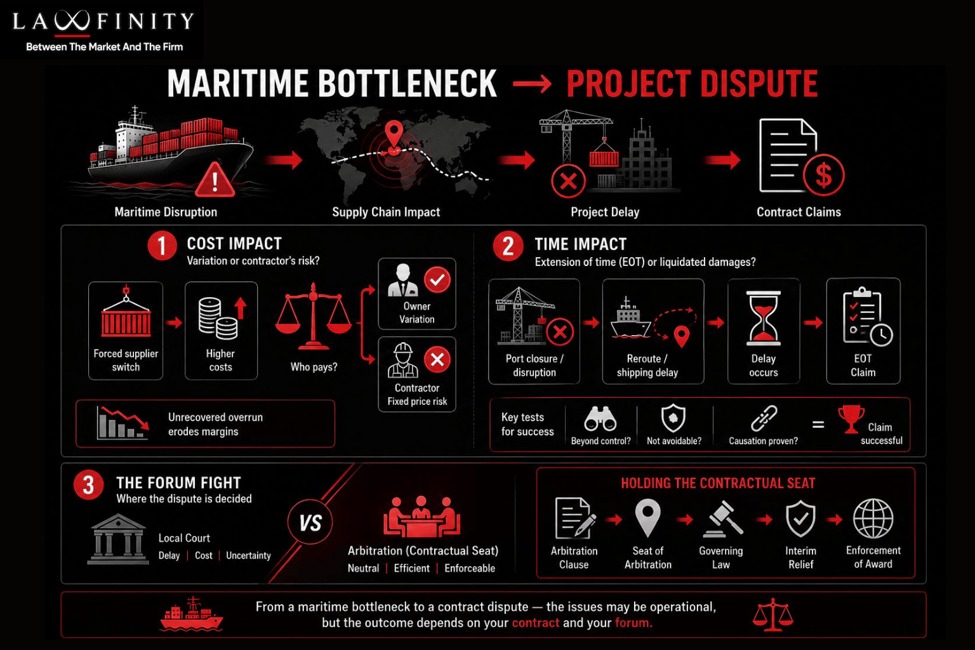

A cost shock at a maritime chokepoint does not stay in the procurement ledger. It travels down the contract, and on a long-gestation infrastructure project it arrives as a claim.

The current disruption in the West Asian sea lanes is the live illustration. Voyage war-risk premiums for Gulf transits have risen sharply, polymer and carbon-input costs have spiked, and container evacuation at gateways such as JNPA has slowed. For a turnkey contractor mid-way through a subcontinental megaproject, each of those is not a market data point. It is the seed of a variation or an extension-of-time claim.

Where the shock becomes a dispute

When a maritime bottleneck reaches a project under a FIDIC or bespoke turnkey form, the fight runs along two well-worn lines.

The first is variation and price adjustment. FIDIC’s Clause 13 (Variations and Adjustments) governs whether a forced switch to costlier, non-chokepoint suppliers is an owner-compensated variation or a cost the contractor swallows. Where the contract is rigidly fixed-price and carries no workable adjustment formula, the contractor absorbs the overrun, and reported margins become paper margins until the claim resolves.

The second is time. To secure an extension of time and escape liquidated delay damages, a contractor must fit a maritime disruption into the force majeure or exceptional-event provisions, Clause 19 in the 1999 Red and Yellow Books, recast as Clause 18, “Exceptional Events,” in the 2017 editions. The argument turns on foreseeability, avoidability and causation: was a chokepoint closure or a shipping-line reroute beyond the parties’ control, and did it in fact cause the delay claimed. That is a forensic, document-heavy contest, and it is where most of these matters are settled.

Behind both sits a forum question. A counterparty facing a slow-burn infrastructure default will often try to pull the matter into a local court to stall it, and counsel on the other side has to hold the contractual seat, which, for cross-border projects, usually means an English- or Singapore-law arbitration clause and the supporting powers of the seat court. Even where a poorly drafted clause fails to explicitly designate a seat, English courts will intervene to save the mechanism; in Chalbury McCouat International Ltd v PG Foils Ltd, the High Court used its powers under Section 18 of the Arbitration Act 1996 to step in and constitute a tribunal via the LCIA after the parties’ own appointment procedure broke down.

The shift that moves the risk

The more durable point is not the shock itself, chokepoints open and close, but what the shock is accelerating.

Faced with execution and working-capital exposure, equipment makers on the corridor are moving away from turnkey EPC, where they carry the completion and logistics risk, toward pure equipment-supply contracts, where they do not. Inox Wind is the cited example, reportedly scaling equipment supply from roughly a quarter of its order book toward three-quarters.

That trade is rational for the manufacturer’s balance sheet. Its consequence is structural: the completion and variation risk does not disappear, it migrates. It lands downstream — on the contractors, developers and international financiers left holding the turnkey obligations without the supplier beside them on the hook. The risk has not been reduced. It has been relocated, and with it, the place where the next dispute will form.

Reading the corridor, not the case

Here the two halves of the market each see only their own. The case-focused firm, in London or in India, is built to run the matter once a project stalls or a guarantee is called and runs it well. The local ally tracks maintainability and tribunal timelines on the file in front of it. Neither is positioned to read the thing that decides who is exposed in the first place: where, across the corridor, completion risk is being shed, where it is settling, and which contract architectures are now carrying risk their drafters did not price.

That is a structural read, not a case read. It does not predict a particular dispute, and it does not need to. It maps where the exposure is migrating and the exposure is migrating now, in the contracts being signed during the shock, long before any of them produces a claim.

The durable point

The sea lanes will clear; war-risk premiums will fall; the chokepoint will reopen. None of that reverses what happened to the contracts signed while it was shut. The completion risk that changed hands stays changed.

A variation claim surfaces when a project stalls and the money runs short. But it was won or lost earlier, when the risk was allocated, in who agreed to carry the completion exposure and on what terms. That is the part worth reading. It is simply not the part that makes the news.

Lawfinity Solutions advises international law firms on cross-border legal market positioning. If the India corridor is a live question for your firm, we would be interested in a conversation. Lawfinity works with one firm per jurisdiction. Engagements begin with a single conversation about your firm’s current position and where the corridor question is live for you. Write to Prachi Shrivastava